Background to Peulwana

Among the challenges that the government has been dealing with in the last two decades are the challenges of poverty, unemployment, and economic exclusion of rural communities. In acknowledgement of the critical role that the agricultural sector can play in dealing with the triple challenges of poverty, unemployment, and economic and social exclusion, the government has put in place and is implementing development programs aimed at bringing smallholder farmers into the mainstream of the agricultural sector and the economy in general.

One of the interventions that the government through the Department of Agriculture and Rural Development has put in place and is implementing is a credit scheme for small-scale and emerging farmers. The program provides short to medium-term input loans to small-scale and emerging farmers who have operational farms. The credit scheme is run by National Credit Regulator (NCR) accredited service providers contracted by the Department of Agriculture and Rural Development. One of the service providers in this regard is Peulwana Agricultural Financial Services.

The Institutional Structure of Peulwana Agricultural Financial Services

Peulwana Agricultural Financial Services is constituted as a private company registered under the Companies Act. It has a board of directors of five members of whom three are non-executive. The board members have extensive experience in management, corporate governance, human resources, and women and gender issues. The company secretary is a legal practitioner.

The company has outsourced accounting functions to an accounting firm and annual financial and system audits are carried out by a duly accredited audit firm.

Peulwana Agricultural Financial Services has a core staff of five people, of whom three are in operation, and the other two are in administration. In addition to the core staff, Peulwana has a list of associates in every province where Peulwana has activities. The associates are called in on a need basis to undertake specific functions as may be needed at that time.

To implement social development projects that will not require the provision of credit, Peulwana has formed a not-for-profit company (NPC). The NPC is managed within Peulwana Agricultural Financial Services, supervised by a board of trustees.

The core objective of Peulwana Agricultural Financial Services is to support small-scale and emerging farmers to develop their farming businesses to become sustainable. Peulwana Agricultural Financial Services:

Provides short to medium-term input loans

Facilitates access to mainstream markets by small-scale and emerging black commercial farmers

Facilitates access to technical support and business development services for funded small-scale and emerging commercial farmers

Taking advantage of the extensive network of on-the-ground associates, service providers, and farmers, Peulwana has as its second objective. In this respect, the focus is on the implementation of agricultural projects in rural areas.

To provide project management services in the implementation of development projects to the government and its development partners.

The core objective of Peulwana Agricultural Financial Services is to support small-scale and emerging farmers to develop their farming businesses to become sustainable. Peulwana Agricultural Financial Services:

Provides short to medium-term input loans

Facilitates access to mainstream markets by small-scale and emerging black commercial farmers

Facilitates access to technical support and business development services for funded small-scale and emerging commercial farmers

Taking advantage of the extensive network of on-the-ground associates, service providers, and farmers, Peulwana has as its second objective. In this respect, the focus is on the implementation of agricultural projects in rural areas.

To provide project management services in the implementation of development projects to the government and its development partners.

What has been Achieved

In the Provision of Input Finance

Peulwana is operating in six provinces. These are Gauteng, North-West, Free State, Limpopo, KwaZulu- Natal, and Northern Cape. From its start in 2009 to about the 1st quarter of 2020, Peulwana reached just over 400 small-scale and emerging farmers and provided them with over R 100 million worth of input loans from a capital base of R 50 million. The supported farmers grow a wide range of crops including different types of grains, potatoes, vegetables, citrus fruits, poultry, grapes, etc.

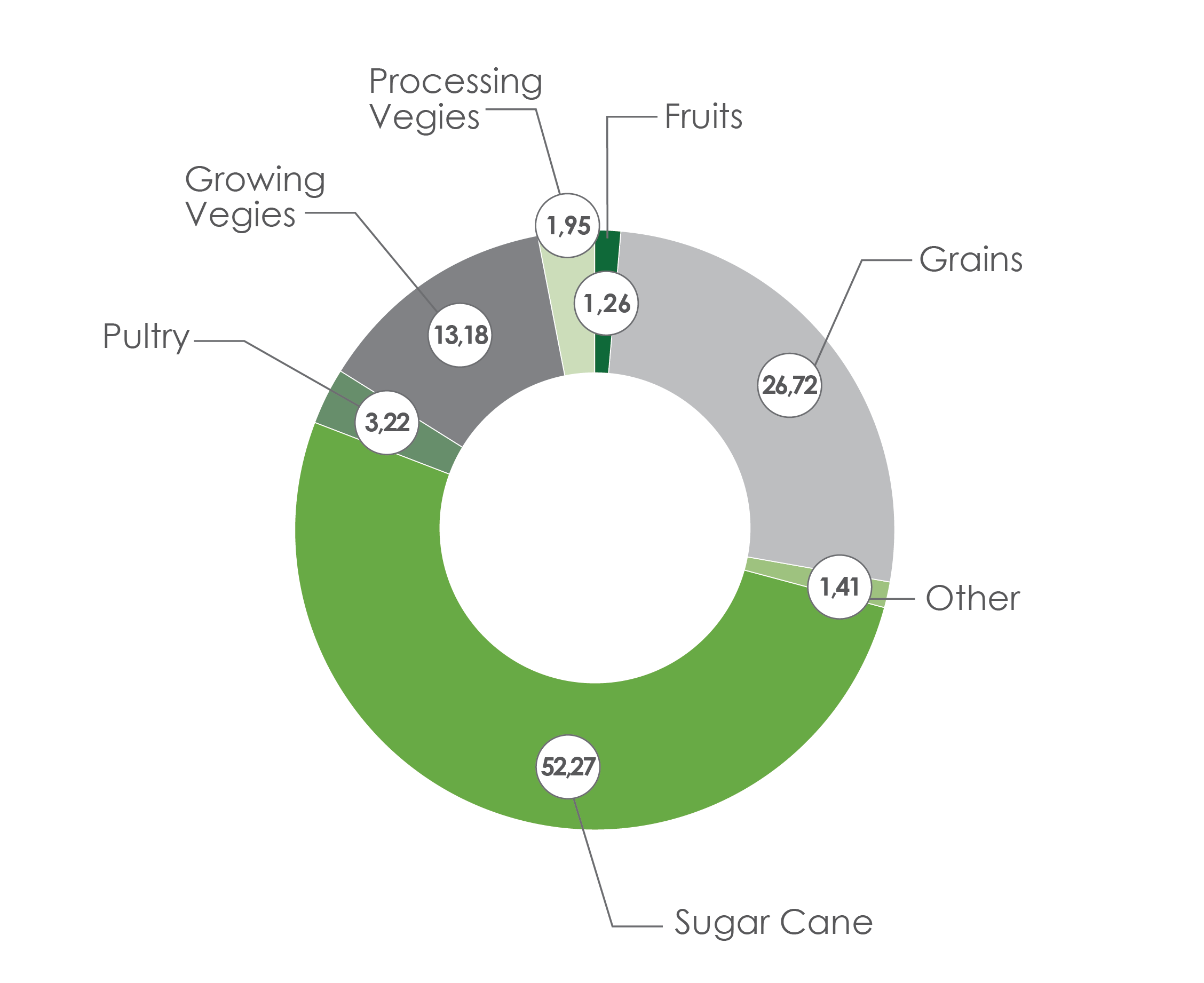

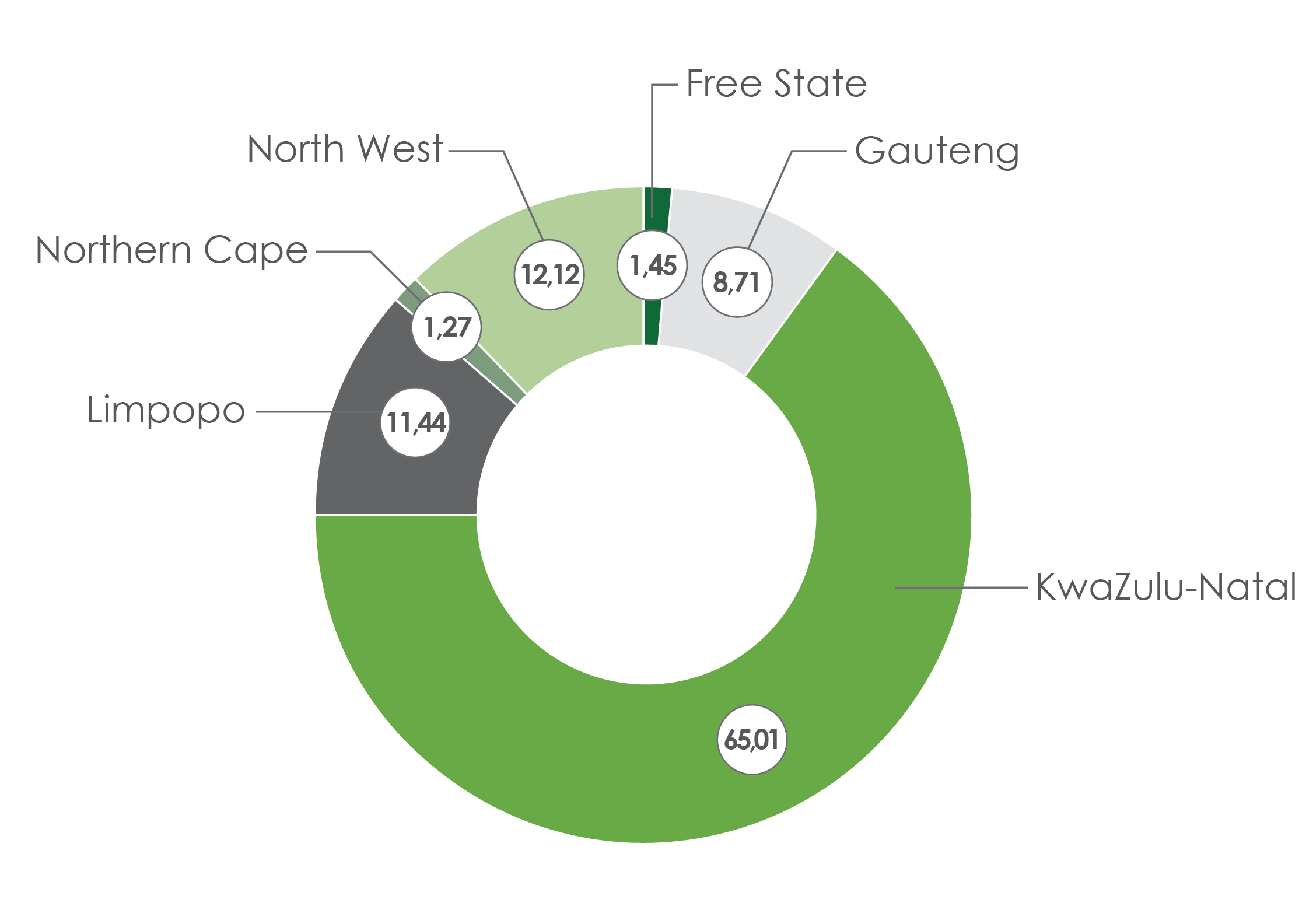

The charts on the right indicate the sectoral distribution and the provincial distribution of loans up to the 1st quarter of 2020.

52 .27 % of the loans were made to sugar cane farmers, followed by 26.72 % of the loans were given to grain farmers.

KwaZulu farmers received 65 % of the loans. These were mostly in sugar cane. Northwest farmers received 12.12 % of the total loans disbursed. These were grain farmers. Limpopo farmers on the other hand received 11.44 % of the total loans given. Nearly all of them are vegetable farmers.

The impact of the provision of input finance to farmers over several years is seen in the farmers who have taken advantage of the support given to them. The impact is reflected in the growth of farms (by size and diversification), in their acquisition of agricultural machinery and equipment, in the development of their technical skills, and in their entry into mainstream markets.

In the Implementation of Development Projects

Peulwana in 2012/2013 and 2013/2014 supported the National Department of Agriculture and Rural Development in the implementation of a food security intervention. In the 2012/2013 season, Peulwana managed a project to cultivate and plant over 1 200 hectares of maize and beans for smallholder households in KwaZulu Natal, Free State, and Northern Cape Provinces.

In the 2013/2014 season, Peulwana managed for the Department of Agriculture a project that designed, produced, and installed grain storage facilities for smallholder households on a pilot basis. The project installed grain storage facilities for smallholder households in the Eastern Cape, Limpopo, and KwaZulu Natal. The households that had the storage facilities installed for them are still (2021) using the facilities.

The Human Resource Capacity of Peulwana Agricultural Financial Services

Peulwana Agricultural Financial Services has a lean full-time staff complement. It has two staff members running the operations of Peulwana. They run the MAFISA credit scheme and provide project management services when Peulwana is contracted to manage a project for the Department of Agriculture, Land Reform and Rural Development. The two staff members are economists with extensive experience in rural development and, for one of them, in marketing and promotion.

A field officer is stationed in Jozini Northern KwaZulu Natal, to support and follow up on the performance and loan repayment of smallholder sugar cane farmers (mostly) in the Makhathini Flats.

Peulwana has in addition, a wide network of associates who are professionals in different fields including soil science, agronomy, plant breeding, agricultural economics, management, marketing and promotion, gender, and traditional affairs. Peulwana also has access to SETA-accredited trainers. When needed, these are called in to provide specialist support in the implementation of projects or the training of farmers.

The office is run by two administrative staff members who manage the loan management information system, keep the books of Peulwana and generally ensure the office is effectively run on a day-to-day basis.

With regard to its governance, Peulwana has a board of directors with skills and experience in diverse areas including management, governance, community, and gender. The board provide guidance and policy direction.

The services of Peulwana can be utilised broadly by any institution/organization that needs or wants to reach rural communities in general and smallholder and emerging farmers in particular. These institutions include:

Government

In the implementation of programs that aim to support the development of smallholder farmers or emerging farmers, the government can make use of Peulwana to implement those programs. The MAFISA input loan scheme and the food security programs described above are good examples.

Corporate companies operating in the agricultural sector

Corporate companies that operate in the agricultural sector are generally ideal partners of Peulwana. There are two bases for the interaction though they are not mutually exclusive.

(a) A corporate company that wants to increase its procurement of inputs from smallholder and emerging farmers both as a commercial decision and as well as its BEEEE compliance can partner with Peulwana to simply aggregate the products (e.g., maize, potatoes, etc.) from smallholder farmers for delivery to the company as an input for processing.

(b) A corporate company that wants to support the production of its input (e.g., wheat, white beans, etc.) by smallholder and emerging farmers can partner with Peulwana through a loan or grant scheme to work with the targeted smallholder or emerging farmers to implement a farmer development program to produce the input the company needs.

Corporate companies operating in rural communities

Peulwana is an ideal partner to a corporate company that is operating in a rural area as part of being a good corporate citizen or meeting one of its license requirements needs to implement programs that contribute to poverty alleviation and employment creation in the communities that are in the catchment areas of the company. Peulwana would design and implement the programs for the company.

Trusts

Peulwana is also an ideal partner to Trusts that have as one of their aims to support the social-economic development of rural communities through the promotion of poverty alleviation and employment creation programs. Peulwana would design and implement such programs for the targeted communities.